Four Reasons to Review Your Life Insurance Needs

You may have purchased life insurance years ago and never gave it a second thought. Or perhaps you don't have life insurance at all and now you need it. When your life circumstances change, you have a fresh opportunity to make sure the people you love are protected.

Marriage

When you were single, life insurance might have seemed like an unnecessary expense, but now someone else is depending on your income. If something happens to you, your spouse will likely need to rely on life insurance benefits to meet expenses and pay off debts.

The amount of life insurance coverage you need depends on your income, your debts and assets, your financial goals, and other personal factors. Even if you have some low-cost life insurance through work, this might not be enough. Buying life insurance coverage through a private insurer could help fill the gap.

Parenthood

When children arrive, revisiting your life insurance needs could help you protect your growing family's financial security. Life insurance proceeds might help your family meet both their current obligations, such as a mortgage, child care, or car payments, and future expenses, including a child's college education. Even if you already have life insurance, children are among the most important reasons to review your policy limits and beneficiary designations.

Retirement

As you prepare to leave the workforce, reevaluate your need for life insurance. You might think that you can do without it if you've paid off all of your debts and feel financially secure. But if you're like some retirees, your financial picture may not be so rosy, especially if you're still saddled with mortgage payments, student loan bills, and other obligations. Life insurance protection could still be important if you haven't accumulated sufficient assets to provide for your family, or you want to replace retirement income lost when you are no longer around.

Life insurance can also be an important tool to help you transfer wealth to the next generation. Or perhaps you're looking for a way to pay your estate tax bill or leave something to charity. You may need to keep some of your life insurance in force or buy a different type of coverage.

Health Changes

A common concern is that life insurance coverage will end if your insurer finds out that your health has declined. But if you've been paying your premiums, changes to your health will not matter.

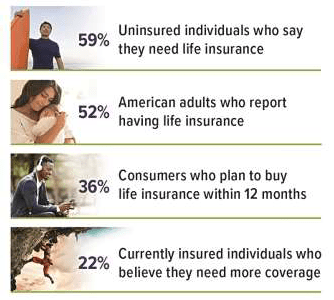

Source: 2021 Insurance Barometer Study,

Life Happens and LIMRA

Some life insurance policies even offer accelerated (living) benefits that you can access in the event of a serious or long-term illness.

You may be able to buy additional life insurance if you need it, especially if you purchase group insurance through your employer during an open enrollment period. Purchasing an individual policy might be more difficult and more expensive, but check with your insurance representative to explore your options.

Of course, it's also possible that your health has improved. For example, perhaps you've stopped smoking or lost a significant amount of weight. If so, you may now qualify for a lower premium.

The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. Before implementing a strategy involving life insurance, it would be prudent to make sure that you are insurable. As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have mortality and expense charges. Any guarantees are contingent on the financial strength and

claims-paying ability of the issuing insurance company. Optional benefits are available for an additional cost and are subject to contractual terms, conditions, and limitations.

Contact our Insurance Agents

Contact our Financial Advisors

To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Non-deposit investment products and services are offered through CUSO Financial Services, LP ("CFS") a registered broker-dealer (Member FINRA/SIPC) and SEC Registered Investment Advisor. Products offered through CFS: are not NCUA/NCUSIF or otherwise federally insured, are not guarantees or obligations of the credit union, and may involve investment risk including possible loss of principal. Investment Representatives are registered through CFS. The Credit Union has contracted with CFS for investment services. Atria Wealth Solutions, Inc. ("Atria") is a modern wealth management solutions holding company. Atria is not a registered broker-dealer and/or Registered Investment Advisor and does not provide investment advice. Investment advice is only provided through Atria's subsidiaries. CUSO Financial Services, LP is a subsidiary of Atria.

Copyright 2006- Broadridge Investor Communication Solutions, Inc. All rights reserved.

Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, or legal advice. The information presented here is not specific to any individual’s personal circumstances.